$40B Wealth Manager to Put "single-digit %" of Portfolio into Bitcoin

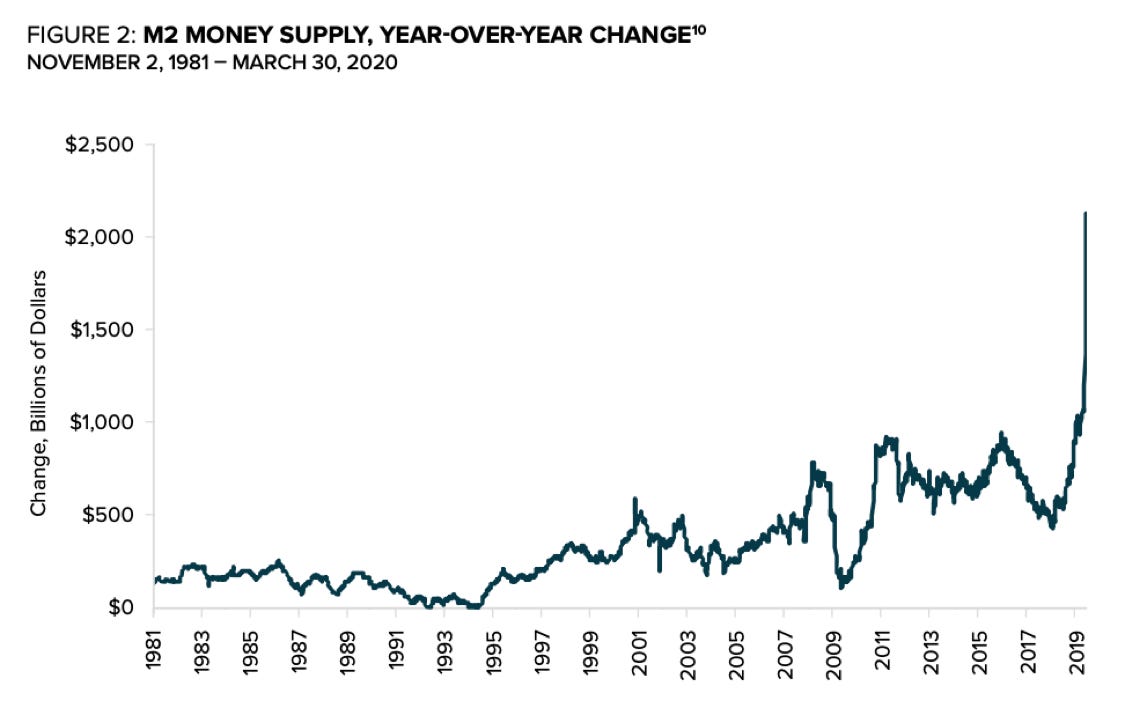

The Great Monetary Inflation

In case you missed it, Paul Tudor Jones, founder of the Tudor Investments Corp hedge fund with nearly $40 billion AUM, announced that he’ll be allocating low single-digit percentages of his portfolio to Bitcoin.

This is a big step in lowering the career risk for other institutional investors seeking to diversify into Bitcoin, as well.

Jones’ thesis largely centered around Bitcoin as a store of value and a hedge against inflation, especially given the current macro environment, although he cited the coming digitization of money everywhere, accelerated by the pandemic, as the most compelling argument to own Bitcoin.

We agree with Jone’s thesis and find it valuable, especially in the context of the macro tailwinds created by this money printing phenomenon.

We’ve expanded and summarized some of Paul’s thoughts below. You can also find the full thesis here.

Outlook: Quantitative Easing vs Quantitative Tightening

There has never been a better time to invest in Bitcoin. Even before COVID-19 hit, we were seeing record levels of money printing as we entered the new decade. Six months later, we’ve soared to new highs of money printing.

Globally, central banks have pumped a record stimulus of $10 trillion dollars into the markets. The U.S. debt to GDP ratio hit a record high of 110% in May, surpassing post World War II levels.

As we take on increasing amounts of debts and attempt to print our way out of the COVID-19 crisis, the mathematically programmed predictability of Bitcoin’s supply curve has never looked better:

“[Bitcoin] is literally the only tradable asset in the world that has a known fixed maximum supply. This brilliant feature of Bitcoin [is] a concept alien to the current thinking of central banks and governments.” – Paul Tudor Jones

PTJ Thesis: Grading Criteria

Bitcoin made the top 4 in Jones’ list of store of value assets. Stores of value were graded on four characteristics: purchasing power, trustworthiness, liquidity, and portability.

“What was surprising to me was not that Bitcoin came in last, but that it scored as highly as it did. Bitcoin had an overall score nearly 60% that of financial assets but has a market cap that is 1/1200th of that. It scores 66% of gold as a store of value, but has a market cap 1/60th that of gold’s. Something appears wrong here, and my guess is it is the price of Bitcoin. – Paul Tudor Jones

Unsurprisingly, the research poll ascribed a purchasing power score of 0 to fiat cash almost across the board. Jones cited Bitcoin as a great way to hedge against the inevitable monetary inflation arising from the central bank’s current approach to monetary policy.

Cash scored the highest on the liquidity scale, though Bitcoin is the only asset the trades 24/7 around the world.

Bitcoin is the clear winner in the portability category. As open-source software, this store of value is a digitally native form of money that moves frictionlessly anywhere in the world at the speed of the internet.

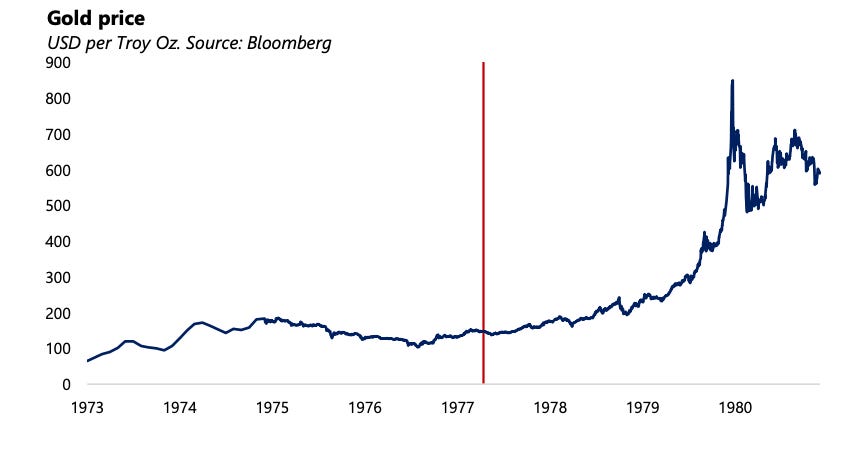

PTJ Thesis: Gold Comparison

Given Jones’ success in the early days of the gold market, we’d be remiss not to touch on his analogous comparison of the two assets.

“Bitcoin reminds me of gold when I first got in the business in 1976. Gold had just been productized as a futures instrument (like Bitcoin recently) and had enjoyed a heck of a bull market, almost tripling in price.”

“But in the case of gold, it was a tremendous buying opportunity, as it went on to more than quadruple past the prior highs. The red line in the chart below shows where we might be in Bitcoin today.”

Onward & upward,

UTXO Management

The information included in this email is based upon information reasonably available to UTXO Management as of the date herein. Furthermore, the information included in this presentation has been obtained from sources the Company believes to be reliable; however, these sources cannot be guaranteed as to their accuracy or completeness.

CONFIDENTIALITY NOTICE: THIS COMMUNICATION IS INTENDED FOR THE INDIVIDUAL OR ENTITY TO WHICH IT’S ADDRESSED. THE INFORMATION CONTAINED HEREIN MAY BE CONFIDENTIAL AND/OR PRIVILEGED INFORMATION. ANY UNAUTHORIZED DISSEMINATION OF THIS EMAIL IS PROHIBITED.